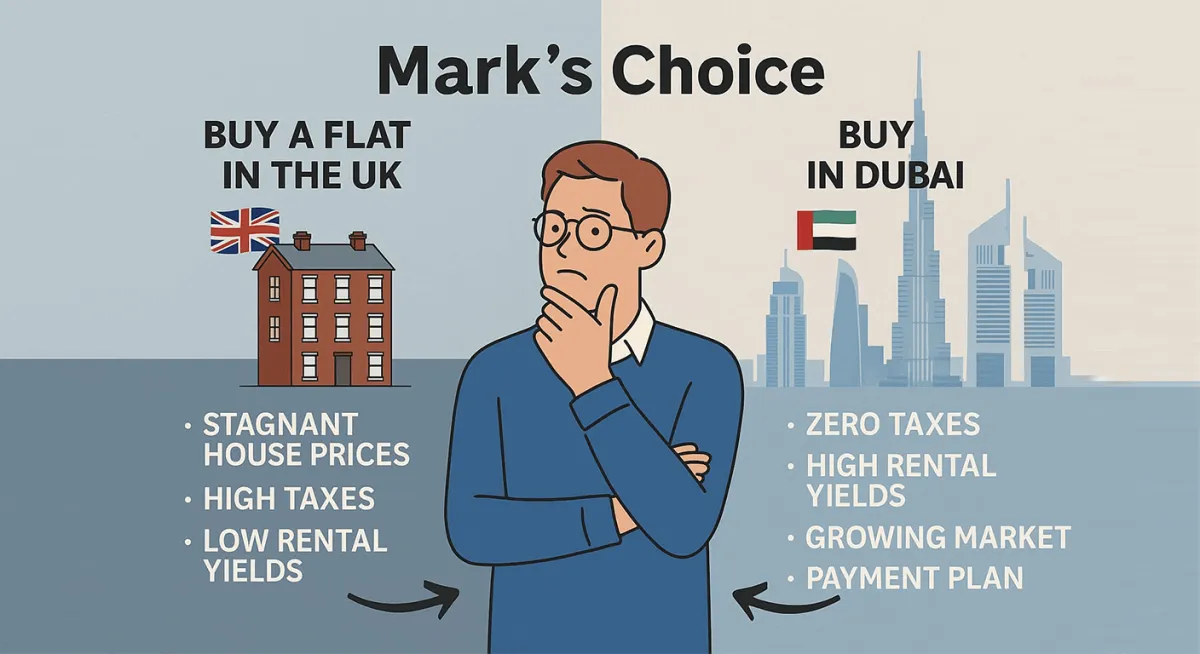

Mark’s £300K Dilemma: UK Property vs Dubai – Where Would You Invest?

Meet Mark, a 42-year-old British professional sitting on £300,000 in savings. After years of watching his UK pension fund crawl and the housing market stagnate, he decides it’s time to invest in real estate.

He has two choices:

Buy a flat in the UK – familiar, but slow returns and high taxes

Explore Dubai – newer market, but growing, tax-free, and globally in demand

Here’s what happens when Mark dives deeper.

Option 1: Buying Property in the UK

Property Price: £300,000

Stamp Duty + Legal Fees: ~£10,000

Rental Yield: ~3.5% = £10,500/year

Tax on Rental Income (20–40%): ~£2,000–£4,000/year

Council Tax + Maintenance: ~£2,000/year

Mortgage? Yes, but with high UK interest rates (now over 5%)

After 5 Years:

Gross earnings: ~£52,500

Net after tax and expenses: ~£35,000–£38,000

Capital Gains Tax & 40% Inheritance Tax apply

House price growth in UK (2023–2024): just -1.3% (Nationwide)

Net outcome: Low yield, high tax, limited growth.

Option 2: Investing in Dubai Real Estate

Mark considers Dubai—and he’s surprised by the flexibility.

20% Down Payment = ~£60,000

NO mortgage needed upfront

Monthly plan: Pay the rest 30–50% over 2–5 years

Post-handover: Flip it, rent it, or take a mortgage

Rental Yield: 8–10% = ~£24,000/year on full value

No Stamp Duty, No Income Tax, No Property Tax

Property price growth in Dubai (2023): 19% average (CBRE)

2024 forecast: 9–12% growth (Knight Frank)

After 5 Years:

£120,000 earned tax-free

Potential resale gain of 20–30%

No inheritance or capital gains tax

Mortgage can be activated later to release cash

Mark realises: Dubai is not just property—it's a strategy.

What Convinced Mark?

UK real estate has stalled

Dubai offers flexibility, zero taxes, and rental demand

He only needs to deploy 20% now and can build the asset gradually

Future exit options: resale, mortgage, or high-yield rental

Brighton to Burj – Built by Someone Like Mark

Mark didn’t know the Dubai market. Until he found Brighton to Burj, a boutique real estate advisory founded by Amit, a British national who lived in the UK for 15+ years.

Amit understood the real pain points:

Inheritance tax

Stamp duty

Market fatigue

Mortgage stress

Legal confusion overseas

Brighton to Burj offers end-to-end guidance tailored for UK-based investors.

FAQs

1. How do rental yields in Dubai compare to the UK for a £300,000 investment?

For a £300,000 investment, a UK property typically offers a rental yield of around 3.5%, which is further reduced by income tax. In contrast, Dubai real estate can provide yields between 8–10% with zero tax on rental income, allowing for significantly higher net earnings.

2. What are the tax implications of investing in Dubai vs the UK?

UK property investments are subject to Stamp Duty, Income Tax (20–40%), Capital Gains Tax, and potential Inheritance Tax. Dubai offers a tax-free environment with no stamp duty, no income tax on rent, and no capital gains or inheritance taxes, making it a more efficient strategy for wealth preservation.

3. Can I invest in Dubai property without a large upfront payment?

Yes, Dubai offers high flexibility through developer-led payment plans. Investors can often start with a 20% down payment (approximately £60,000 for a £300,000 property) and pay the remaining balance over 2 to 5 years, often without needing a mortgage upfront.

4. What has been the capital growth trend for Dubai property compared to the UK?

While the UK housing market has seen periods of stagnation or slight decline (e.g., -1.3% in 2023-2024), Dubai's property market saw an average growth of 19% in 2023, with continued forecasts for high single-digit or double-digit growth in 2024 and 2025.